The Sovereign Engine: Architecting Financial Inclusion Through AI, Blockchain, and the Democratization of Capital

The Undervalued Engine: Why Alternative Platforms Matter for Underrepresented Founders

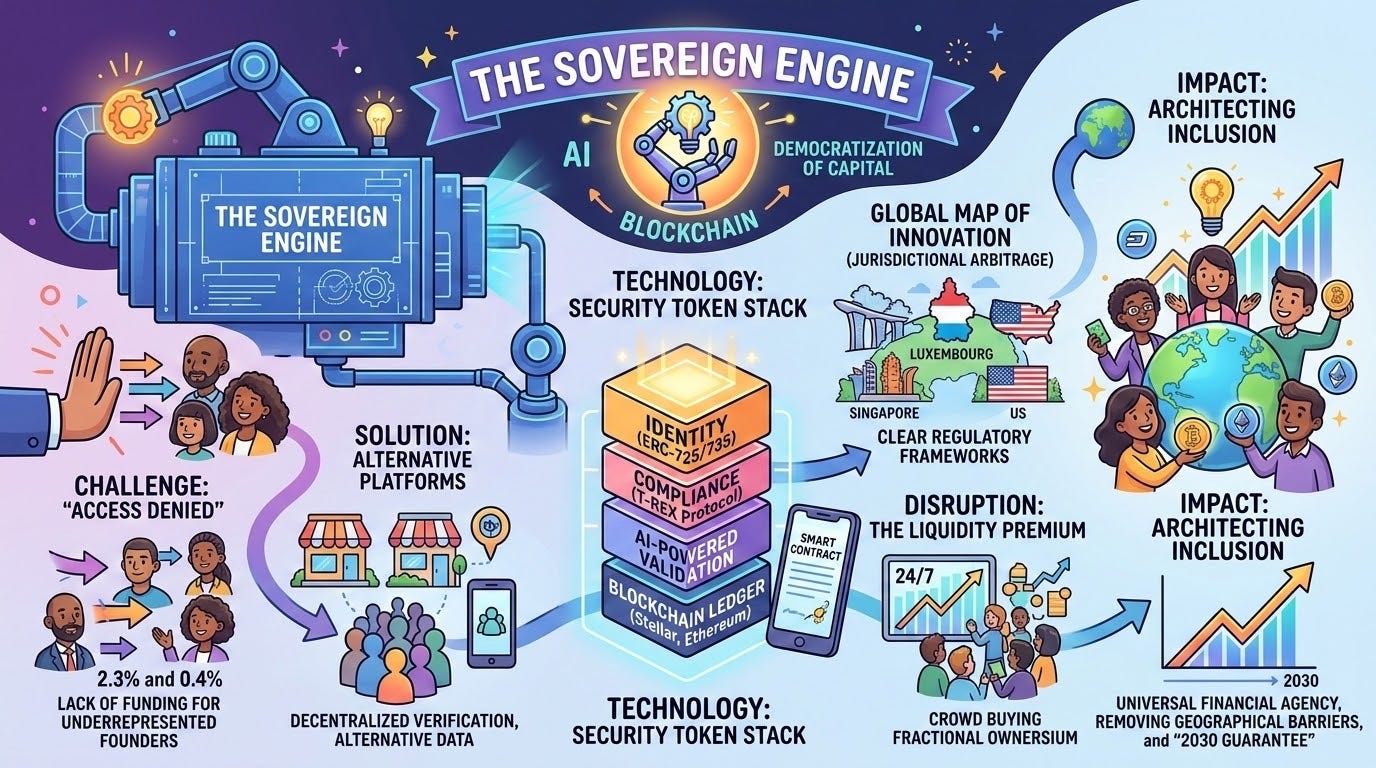

To solve the historical inequities in venture capital, we propose the “Sovereign Engine”, a conceptual framework integrating AI-driven underwriting with blockchain-based settlement to automate and democratize capital formation.

The current narrative of venture capital is one of historical pattern matching, a closed loop where capital flows to founders who mirror the image of those who came before them. For decades, this system has operated with a “gatekeeper” mentality, relying on warm introductions and proximity to established hubs like Silicon Valley or New York. The data is sobering: in 2024, female-only founding teams received just 2.3% of global venture capital funding. Similarly, funding for Black-founded startups remains critically low; in 2024, these ventures received just 0.4% of total U.S. venture funding. This is not a lack of viable ideas, but a failure of the architecture.

This systemic exclusion, often manifesting as an “Access Denied” error in economic mobility, imposes a massive drag on the global economy. Research from the Nasdaq Economic Institute indicates that including more women and Black Americans in the early stages of innovation could boost US GDP by $640 billion. When we ignore underrepresented founders, we are not just failing to promote fairness; we are leaving significant economic potential on the table.

Alternative financial platforms like crowdfunding, peer-to-peer (P2P) lending, and blockchain-enabled asset marketplaces, are the primary tools for breaking this cycle. Unlike traditional venture capital, which relies on opaque networking, alternative platforms focus on decentralized verification and data-driven analysis. This evolution, the “Agentic Revolution”, marks the shift toward autonomous, AI-driven financial workflows, moving from passive reliance on gatekeepers toward proactive, programmable execution.

By utilizing alternative data, such as mobile money transactions, digital payment histories, and platform records, new scoring models can evaluate creditworthiness for the “credit invisible.” This is not charity; it is efficient capital allocation. Platforms like Gojo & Company demonstrate this scalability, leveraging tech-operational capacity to extend inclusion where legacy banks historically could not.