The Invisible Bridge: Why the Future of Money is Inclusive by Design

The Finale of a Four-Part Series on Financial Architecture and Human Dignity

We have spent the last three chapters of this journey dissecting the “Walled Garden” of global finance. We have analyzed the “Poverty Tax” that drains billions from the underbanked. We have marveled at the cryptographic “magic” of Zero-Knowledge Proofs and the democratization of high-yield assets. But as we stand at this threshold, we must recognize that we are not merely discussing a change in ledger technology. We are witnessing the birth of a new social contract.

In this final installment, we look beyond the whiteboards and the code repositories to see the world that these technologies are quietly building. As a futurist and macroeconomist, I see a horizon where the friction of the legacy system has been replaced by an “Invisible Bridge”—a financial infrastructure so seamless and ubiquitous that we forget it exists, much like we forget the TCP/IP protocols that power our digital lives.

2030: The Death of the Zip Code

Imagine a Tuesday morning in October 2030. A freelance graphic designer in a rural town in Ohio, a migrant worker in a suburb of Paris, and a small-scale coffee farmer in the highlands of Ethiopia all wake up to the same reality: their geographic location no longer dictates their economic potential.

In 2030, the word “blockchain” is rarely mentioned in casual conversation. It has become the invisible backbone of the global economy. The “Walled Garden” we once lamented—where access was a privilege of the elite—has been dismantled. The traditional credit score, once a biased and opaque gatekeeper based on historical data from centralized bureaus, has been replaced by a “Sovereign Financial Passport”.

The New Financial Citizenship

In this future, your financial identity is portable and private. Using Decentralized Identity (DID) and Zero-Knowledge Proofs (ZKPs), individuals prove their reliability through a “green light” system. They no longer surrender their Social Security Numbers or entire bank histories to prove they can afford a $200 micro-loan. Instead, the network verifies their consistent utility payments and rent—routine behaviors that the legacy system ignored for decades.

This is the end of “banking deserts.” In 2030, the “Zip Code Discrimination” that once plagued Low-to-Moderate Income (LMI) households in the United States is a relic of the past. Access to capital is no longer a function of which physical branch is on your corner, but of the verifiable truth of your economic participation.

The Great Convergence: AI and the Distributed Ledger

The most profound shift of the next decade will not be blockchain alone, but its convergence with Artificial Intelligence. If blockchain is the “immutable memory” of the future economy, AI is its “analytical brain.” For the 1.4 billion unbanked and the millions of underbanked families in developed markets, this nexus provides the ultimate tool for social mobility.

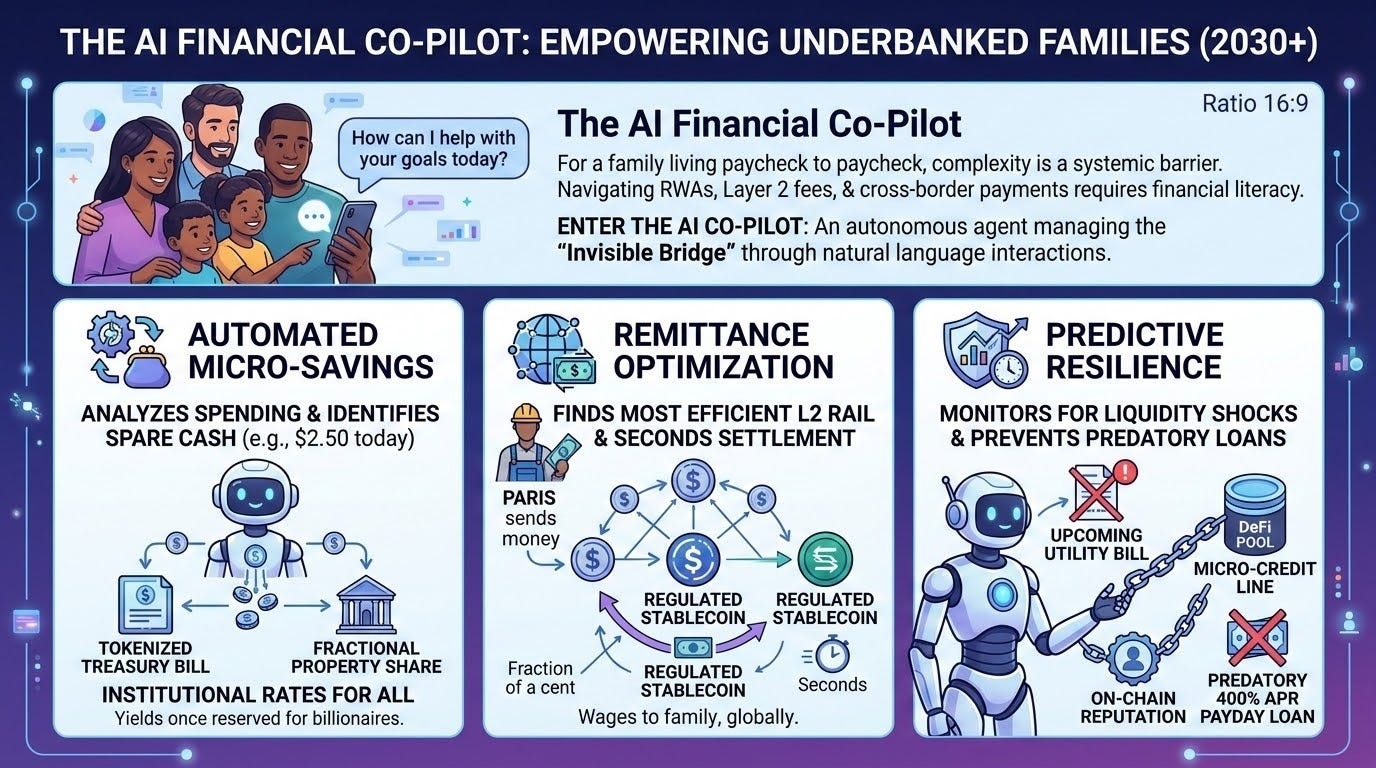

The AI Financial Co-Pilot

For a family living paycheck to paycheck, the complexity of modern finance is a systemic barrier. Navigating high-yield Real World Assets (RWAs), managing Layer 2 gas fees, and optimizing cross-border remittances requires a level of “financial literacy” that most people simply don’t have the time to acquire.

Enter the AI Financial Co-Pilot. In 2030, underbanked families interact with their finances through natural language. An autonomous agent, tailored to the family’s specific goals, manages the “Invisible Bridge” for them.

Automated Micro-Savings: The AI analyzes spending patterns and identifies that a family can spare $2.50 today. It instantly routes that $2.50 into a tokenized Treasury bill or a fractional share of a high-yield property, earning institutional rates that were once reserved for billionaires.

Remittance Optimization: When a worker in Paris sends money home, the AI automatically selects the most efficient Layer 2 rail, converts the wages to a regulated stablecoin, and settles the transaction in seconds for a fraction of a cent.

Predictive Resilience: The AI monitors for potential liquidity shocks. If it detects an upcoming utility bill that the account cannot cover, it can automatically negotiate a micro-credit line from a DeFi pool, using the user’s on-chain reputation as collateral, preventing the predatory 400% APR payday loans of the legacy era.

Blockchain: The Truth-Layer for AI

The danger of AI has always been its potential for “hallucination” or manipulation. In a financial context, an AI that misrepresents data could be catastrophic. This is where the blockchain becomes essential.

Blockchain serves as the verifiable source of truth for the AI. Every data point the AI uses to make a decision—every rent payment, every yield distribution, every regulatory attestation—is anchored on a transparent, immutable ledger. The AI cannot “invent” a credit history because the blockchain provides a cryptographically signed record of reality. This creates a feedback loop of trust: the AI provides the accessibility, while the blockchain provides the accountability.

Summarizing the Journey: From the Wild West to Universal Utility

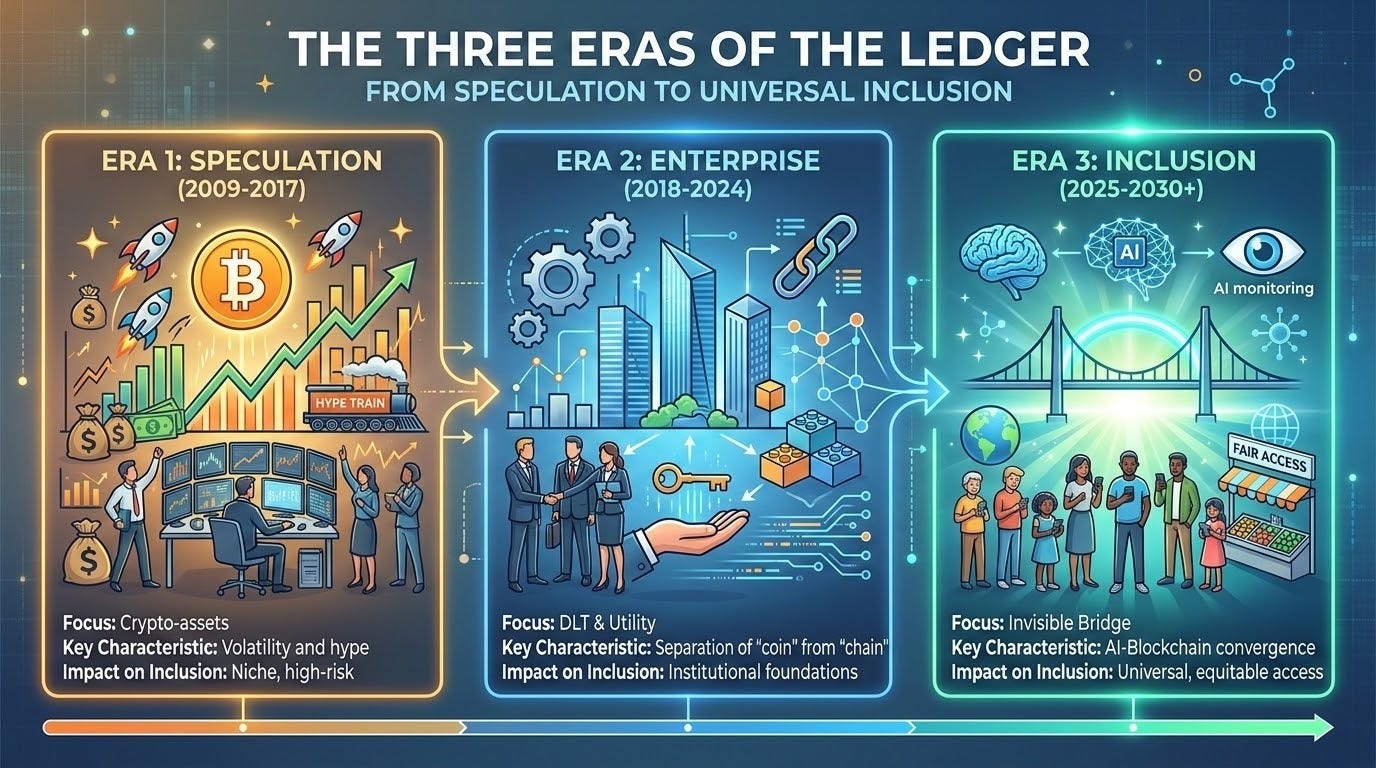

As we close this series, it is vital to reflect on how far we have traveled. We began this exploration by acknowledging that blockchain was born in a “Wild West” of speculation. For years, the public narrative was dominated by volatile assets and “get-rich-quick” schemes that often obscured the underlying technological breakthrough.

We have moved from a niche technology associated with rebellion to a robust, utility-driven infrastructure capable of solving the world’s most persistent economic failures. We have transitioned from “buying trust” from expensive intermediaries to “inherent trust” within the architecture itself.

The journey from Blockchain’s Evolution to Breaking the Gilded Cage articles has been a progression from the possibility of change to the technical certainty of it. We have seen that the “Gilded Cage” is not a law of nature; it is a design choice. And design choices can be changed.

A Moral Imperative: The Architecture of Equality

The case for an inclusive financial design is not merely an economic one; it is a moral one. Financial exclusion is a “structural wealth drain” that strips dignity from communities. When we force a migrant worker to lose five hours of labor to a remittance fee, we are not just taking their money; we are taking their time, their effort, and their ability to provide for their children.

Innovation is the most powerful tool we have for social mobility. By building the “Invisible Bridge,” we are ensuring that the math of wealth creation is identical for every human being on the planet. We are moving toward a world where “financial freedom” is a technical guarantee, not a political promise.

Call to Action: The Architects of the Future

To the developers in the room: Your code is the new law. You have the power to embed equity into the very foundation of the global economy. Prioritize the user experience of the underbanked. Build for the “credit invisible.” Remember that a protocol that only serves the wealthy is just a digital version of the old “Walled Garden”. Use modularity and Layer 2s to drive the cost of participation to zero.

To the regulators: The goal should not be to protect the incumbents of the past, but to protect the citizens of the future. Embrace “Regulation as Code”. Clear frameworks like MiCA prove that we can have both innovation and consumer protection. Do not let the fear of the new prevent the dismantling of the extractive old.

The “Invisible Bridge” is being built today. It is built every time a ZK-Proof is generated, every time an RWA is tokenized, and every time a cross-border payment is settled for pennies. The walls are coming down. The future of money is inclusive, it is sovereign, and it is finally designed for all of us.

Let’s build it.

Citations and Sources

World Bank Group. (2022). The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. https://globalfindex.worldbank.org/

International Monetary Fund (IMF). Staff Discussion Notes on Financial Inclusion. https://www.imf.org/en/Publications/Search?series=Staff+Discussion+Notes&publicationtype=Staff+Discussion+Notes&Topics=Financial+Inclusion

Federal Deposit Insurance Corporation (FDIC). 2023 National Survey of Unbanked and Underbanked Households. https://www.fdic.gov/analysis/household-survey/

European Parliament. (2023). Regulation (EU) 2023/1114 on Markets in Crypto-assets (MiCA). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32023R1114

McKinsey & Company. (2023). Tokenization: A digital-asset déjà vu. https://www.mckinsey.com/industries/financial-services/our-insights/tokenization-a-digital-asset-deja-vu

Circle Official Reports. (2025). The State of the USDC Economy. https://www.circle.com/en/transparency

Decentralized Identity Foundation (DIF). Core Specifications and Architecture. https://identity.foundation/

The Brookings Institution. Economic Policy Research on the Poverty Tax. https://www.brookings.edu/topic/economic-policy/

Nakamoto, S. (2008). Bitcoin: A Peer-to-Peer Electronic Cash System. https://bitcoin.org/bitcoin.pdf

World Bank Group. (Ongoing). Remittance Prices Worldwide (RPW) Database. https://remittanceprices.worldbank.org/