The CLARITY Act: An Overview of US Regulatory Changes

Is This The Future Architecture of Equality?

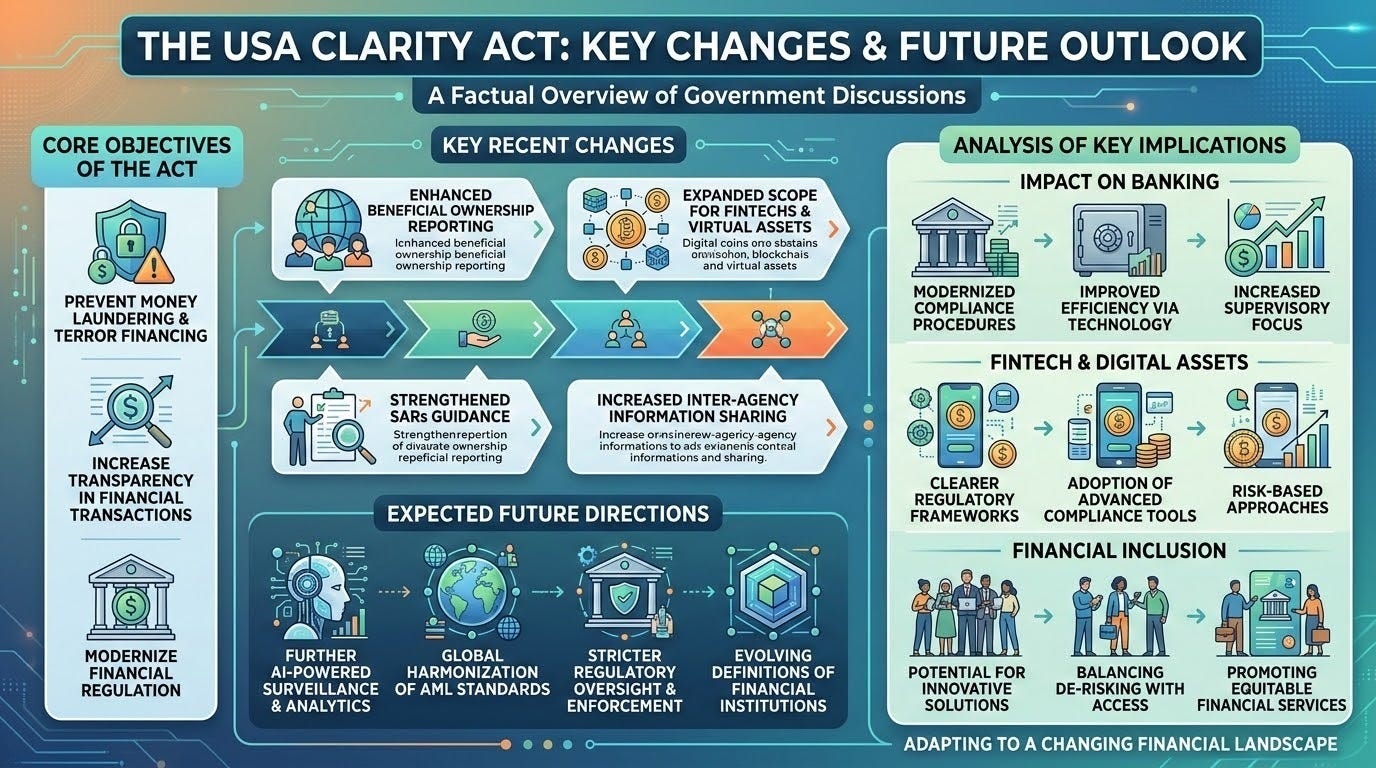

The CLARITY Act introduces structural changes to the financial landscape in the United States. Following a period where regulatory oversight for digital assets was primarily through enforcement and interpretation of older standards like the 80-year-old Howey Test, the Act establishes a clear federal framework for stablecoins and digital assets. This shift from an uncertain “Regulation by Enforcement” approach toward a defined structure is intended to promote domestic innovation and provide regulatory certainty.

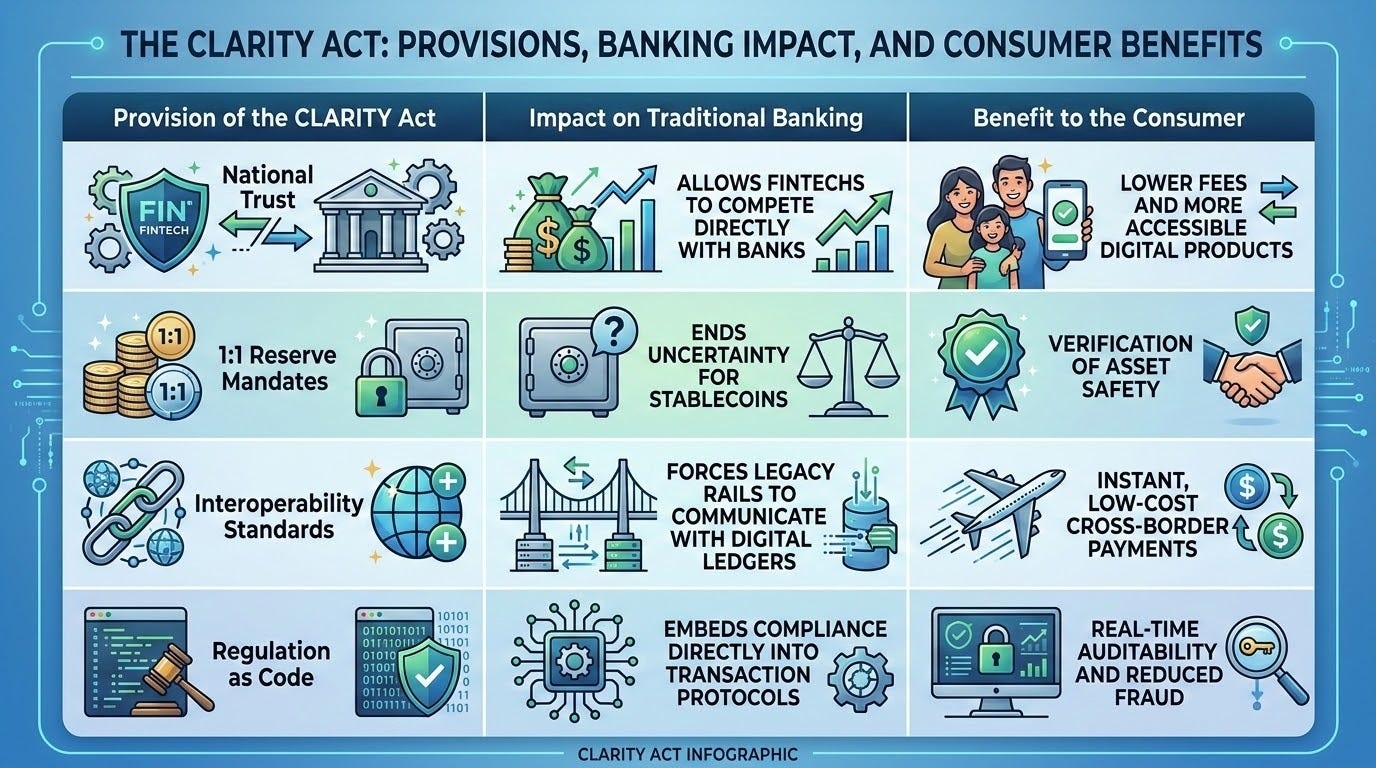

The Act, alongside its 2025 predecessor the GENIUS Act, creates a federal structure for stablecoins and digital assets. This structure includes mandates moving toward a standard that requires 1:1 backing for stablecoins, which is designed to be verifiable on-chain in real-time.

Impact on Banking

The traditional banking sector is facing evolution due to these new regulatory changes. Historically, certain households, particularly Low-to-Moderate Income (LMI) households, have faced barriers to entry due to practices such as high minimum balance requirements and punitive overdraft fees. The CLARITY Act addresses this by providing clear regulatory pathways for non-bank institutions to obtain National Trust Charters. This measure is intended to foster a more competitive environment for financial services.

Fintech and Compliance Innovation

A significant shift for fintech innovators involves the integration of regulatory compliance directly into technological solutions, often referred to as “Regulation as Code.” In the past, scaling financial products across jurisdictions required substantial legal fees and large compliance teams. The CLARITY Act incentivizes the embedding of compliance rules, such as Anti-Money Laundering (AML) and Know-Your-Customer (KYC) standards, directly into smart contracts, creating a framework intended to be more efficient and scalable.

Financial Inclusion

Financial inclusion efforts aim to reduce the excessive costs paid by an estimated 63 million Americans to manage their money. These costs include:

Paycheck Cashing: Can cost 3-5% of the value.

Remittances: Can cost up to 10% for sending money home.

Payday Loans: Can result in cycles with up to 400% APR.

The CLARITY Act supports technologies intended to mitigate these costs by empowering tools such as:

Decentralized Identity (DID): This technology enables individuals classified as “credit invisible” to establish creditworthiness by using non-traditional data, such as utility and rent payments.

Low-Cost Payment Rails: By legitimizing stablecoins within a defined framework, the Act seeks to reduce the marginal cost of financial transactions toward zero, creating a more secure, 24/7 financial layer.

Tokenized Real-World Assets (RWAs): Households can access automated micro-savings mechanisms that compound instantly in tokenized RWAs, offering rates previously restricted to institutional investors.

Future Expected Changes

While the Act provides a current framework, potential legislative updates are anticipated to focus on three key areas:

AI and Credit Underwriting

Future amendments may formalize the role of Artificial Intelligence (AI) in credit underwriting. This focus would likely include new standards for AI transparency to ensure that algorithmic bias is not integrated into new credit models.

Interoperability with CBDCs

As pilots for public-sector digital currencies, such as the Digital Euro and potential Digital Dollar, mature, the CLARITY Act may evolve to ensure seamless interoperability between private-sector stablecoins and these central bank digital currencies (CBDCs).

Global Regulatory Harmonization

The Act is already aligning with international frameworks such as the EU’s MiCA standards. Future legislative steps are expected to work toward harmonization, potentially creating a structure where Decentralized Identity (DID) verification in the U.S. is recognized internationally.

Conclusion: The Architecture of Equality

As we stand in the mid-point of 2026, the global financial landscape is no longer the “Wild West” of speculation we once navigated. The “Gilded Cage” of traditional banking, a system that for decades prioritized extraction and control over universal access is finally being dismantled not by a single strike, but by the steady, immutable logic of code and the legislative force of the CLARITY Act.

We have spent years discussing the “Invisible Bridge” that technology could build. We marveled at the cryptographic magic of Zero-Knowledge Proofs (ZKPs) and the potential for a “Sovereign Financial Passport.” But until now, these were architectural dreams held back by the friction of legacy regulation. The CLARITY Act represents the first true structural blueprint for a future where money is inclusive by design, and where the “Poverty Tax” that drains $31 billion annually from American families is finally rendered obsolete.

The case for the CLARITY Act is not merely economic; it is a moral one. Financial exclusion is a structural wealth drain that strips dignity from communities. When we build a system that requires a migrant worker to lose five hours of labor to a fee, we are not just taking their money; we are taking their time and their children’s future.

Innovation is the most powerful tool we have for social mobility. The CLARITY Act is the blueprint for a world where “financial freedom” is a technical guarantee, not a political promise. We are moving toward a 2030 where “blockchain” is no longer a buzzword, but the invisible, equitable backbone of a global economy that serves all of us.

The walls are coming down. The bridge is being built. It is time to embrace the architecture of equality.

Citations and Sources

Federal Deposit Insurance Corporation (FDIC). (2023). National Survey of Unbanked and Underbanked Households. https://www.fdic.gov/analysis/household-survey/

Consumer Financial Protection Bureau (CFPB). Data Point: Credit Invisibles. https://www.consumerfinance.gov/data-research/research-reports/data-point-credit-invisibles/

European Parliament. (2023). Regulation (EU) 2023/1114 on Markets in Crypto-assets (MiCA). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32023R1114

World Bank Group. (2022). The Global Findex Database 2021. https://globalfindex.worldbank.org/

Circle Official Reports. (2025). The State of the USDC Economy. https://www.circle.com/en/transparency

Decentralized Identity Foundation (DIF). Core Specifications and Architecture.

International Monetary Fund (IMF). Financial Development and Inclusion. https://www.imf.org/en/Publications/fandd/issues/2016/june/caruana

Pew Charitable Trusts. Payday Loan Facts and the CFPB’s Authority. https://www.pewtrusts.org/en/research-and-analysis/reports/2016/05/payday-loan-facts-and-the-cfpbs-authority

Finovate News. (2026). 5 Things to Know about the CLARITY Act.https://finovate.com/5-things-to-know-about-the-clarity-act/

While there is still immense work to be done, no progressive economy can afford to ignore or fear structural technology. Incumbents will inevitably lobby against disruption because they are heavily capitalized in legacy systems. Anything that shifts power back to the consumer or lowers competitive barriers to entry threatens their positioning, frequently leading to institutional resistance at the expense of collective well-being. The path forward requires a cautious but decidedly optimistic embrace of innovation, not a retreat into fear.