From Shared Ledgers to Intelligent Agents: The Architectural Paradigm Shift

The Agentic Revolution: How Blockchain’s Truth and AI’s Execution Dismantle the Gilded Cage of Global Finance.

The transition from passive ledgers to autonomous AI agents represents a fundamental architectural leap that moves finance from mere record-keeping to proactive execution. While blockchain provides the immutable, permissionless rails for value, AI agents solve the terminal friction of user complexity and financial literacy that legacy institutions have weaponized to maintain dominance. This analysis details why this convergence is the only viable path to dismantling the “Poverty Tax” and engineering a truly inclusive 21st-century economy.

Macro Framework & Market Realities

The global financial system is currently characterized by a profound irony: the more “digital” banking becomes, the more exclusive it remains for the vulnerable. I categorize the last decade as the era of “Fintech 1.0,” a period where sleek user interfaces were built on top of the same exclusionary legacy banking rails. These institutions—neo-banks and digital wallet providers—attempted to bridge the gap but ultimately hit the same structural walls regarding unit economics and cross-border friction. They relied on the same SWIFT networks and centralized clearinghouses that have historically marginalized 1.4 billion unbanked adults worldwide.

My analysis reveals that the primary failure of the current system is not a lack of technology, but the persistence of a “Poverty Tax.” In the United States alone, the underbanked are stripped of an estimated $31 billion annually through predatory alternative financial services. These include paycheck cashing fees of 3-5%, remittance costs reaching 10%, and payday loans with Annual Percentage Rates (APRs) often hitting 400%. This is not a service fee; it is a structural wealth drain that removes the very oxygen community growth requires.

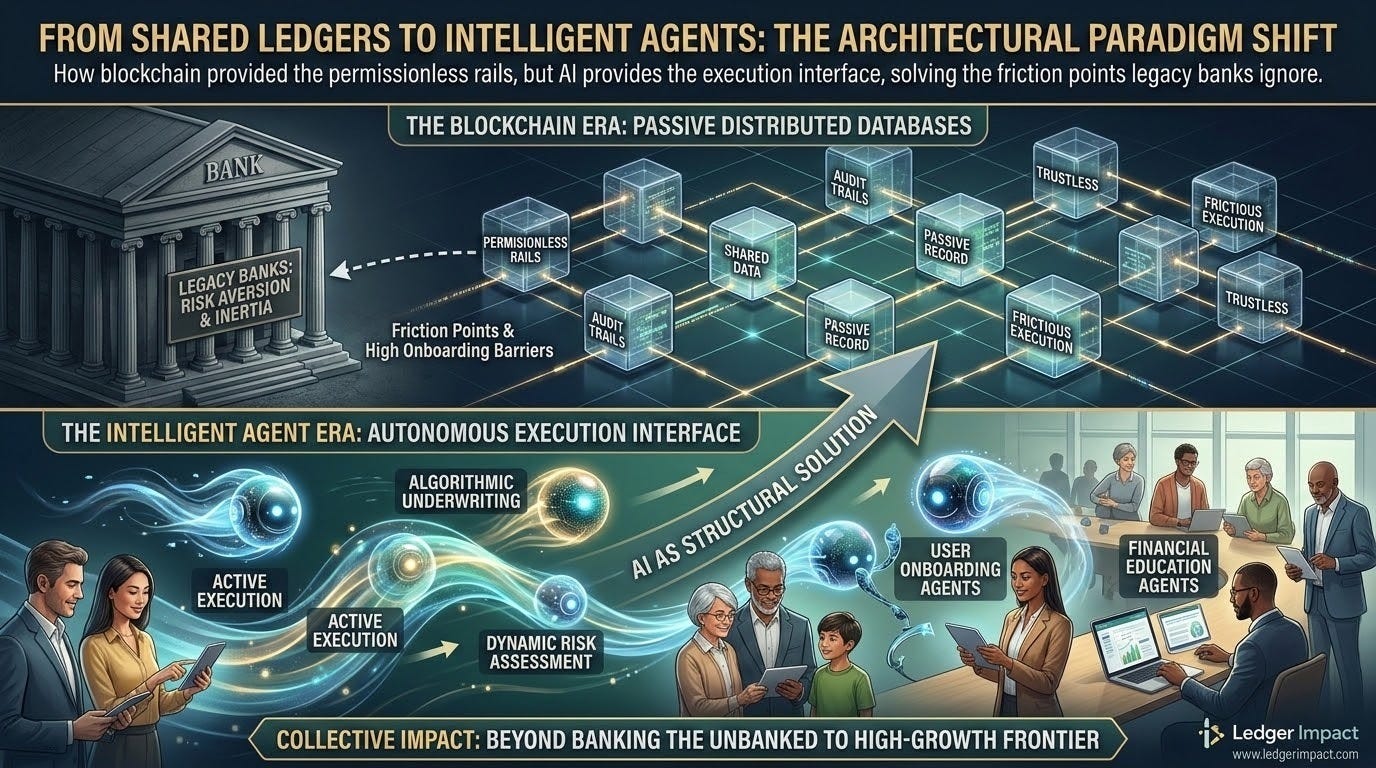

Blockchain technology was introduced as a remedy, offering “permissionless rails” and “inherent trust” within the architecture itself. However, I argue that blockchain alone was insufficient. While it solved the “Truth” problem—providing an immutable ledger—it failed to solve the “Utility” problem. For a family living paycheck to paycheck, managing Layer 2 gas fees, private keys, and cross-border remittance rails requires a level of financial literacy that constitutes a new barrier to entry. The ledger is a passive database; it records reality but does not change it. To truly bank the unbanked, we must move from passive storage to active, intelligent execution.

Structural Deep Dive: The Agentic Revolution

The architectural shift I am highlighting is the move toward the AI Financial Co-Pilot. In this model, blockchain serves as the “Truth-Layer,” providing a verifiable source of reality for an autonomous agent. Every data point—from rent payments to yield distributions—is anchored on a transparent ledger, ensuring the AI cannot “invent” a credit history. This creates a feedback loop of trust where the AI provides accessibility while the blockchain provides accountability.

The Mechanics of Intent-Based Finance

The transition to active systems involves three core technical pillars that I have identified as critical for founders and investors to understand:

The efficiency of this model is best illustrated through the “Invisible Bridge.” My research shows that by 2030, underbanked families will interact with their finances through natural language interfaces. An autonomous agent, tailored to a family’s specific goals, will manage the complexity of the global financial grid on their behalf.

For example, an agent can perform Automated Micro-Savings. By analyzing spending patterns, the AI might identify that a family can spare $2.50 today. It instantly routes that amount into tokenized Real-World Assets (RWAs), such as Treasury bills or fractional shares of high-yield property. This allows individuals with minimal savings to participate in asset classes previously reserved for institutional investors, earning rates that were once the exclusive domain of billionaires.

Furthermore, Remittance Optimization becomes a background process. When a worker sends money home, the AI automatically selects the most efficient Layer 2 rail, converts the wages to a regulated stablecoin, and settles the transaction in seconds for a fraction of a cent. This dismantles the “black box” of legacy infrastructure where migrant workers often lose 5% to 10% of their wages to hidden fees.

Predictive Resilience as a Sovereign Tool

The most profound impact of agentic finance is what I call “Predictive Resilience.” The AI monitor identifies potential liquidity shocks before they occur. If a utility bill is upcoming and funds are insufficient, the agent can automatically negotiate a micro-credit line from a DeFi pool, using the user’s on-chain reputation and rent payment history as collateral. This prevents the descent into the predatory 400% APR payday loan cycles that define the current era. In this framework, AI is not a corporate tool for marketing; it is a sovereign infrastructure tool for survival and growth.

The Leadership and Culture Mandate

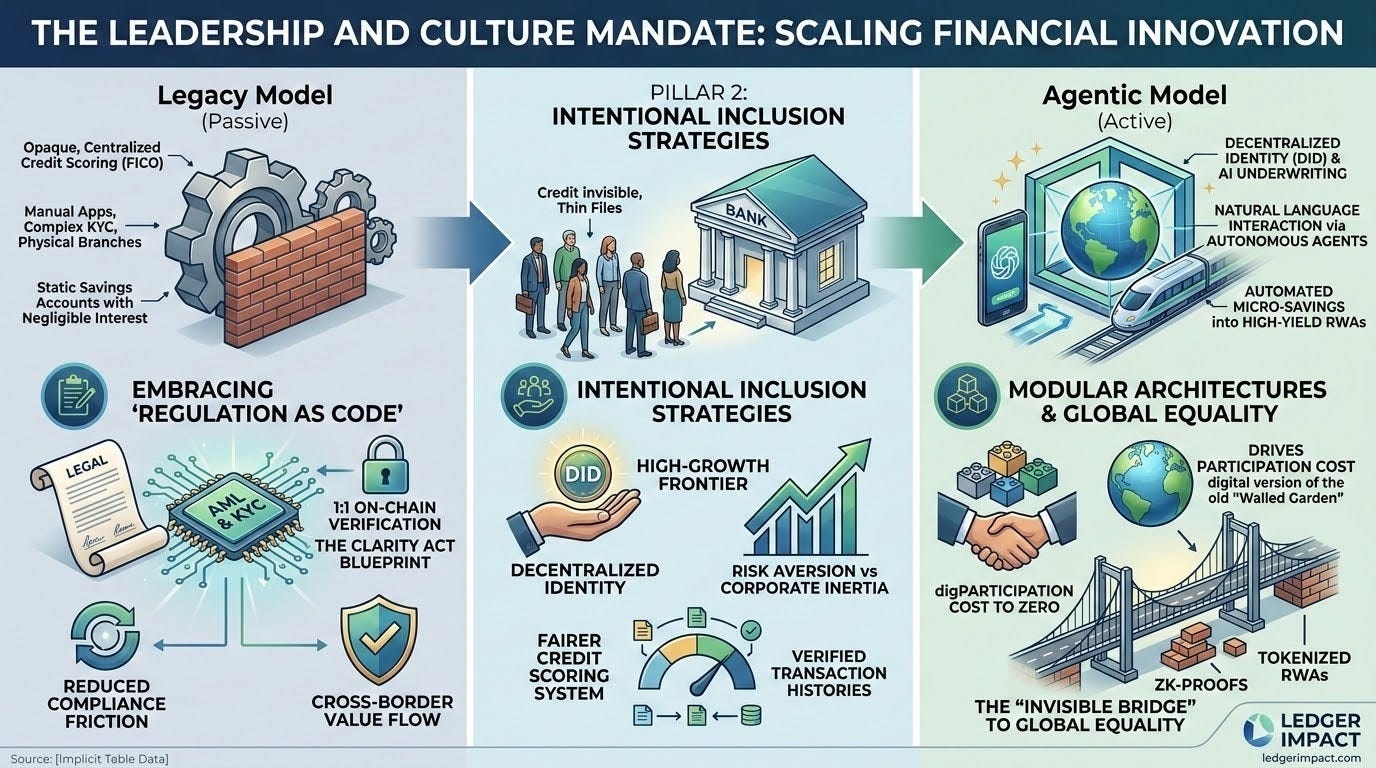

For founders and executive leaders, scaling this solution requires a radical management pivot. We are no longer in the business of building “features”; we are in the business of training “agents.” This requires a shift from a product-centric culture to a system-centric culture.

Embracing “Regulation as Code”

Leaders must champion the integration of regulatory compliance directly into technological solutions—a concept I refer to as “Regulation as Code”. The CLARITY Act serves as a blueprint for this shift, establishing a federal framework for stablecoins that mandates 1:1 backing verifiable on-chain in real-time. Historically, scaling across jurisdictions required massive legal teams; tomorrow’s winners will embed Anti-Money Laundering (AML) and Know-Your-Customer (KYC) standards directly into smart contracts. This reduces the friction of compliance and allows for the seamless, cross-border flow of value.

Intentional Inclusion Strategies

Founders must prioritize the “credit invisible”—those with thin files at centralized bureaus. This is not a charity play; it is a high-growth frontier. My analysis suggests that the legacy system’s “risk aversion” is often just a mask for corporate inertia and a desire to protect monopoly-like business models. By using Decentralized Identity (DID) to verify transaction histories, founders can build a fairer credit scoring system where none existed before.

Investors should look for “modular” architectures that drive the cost of participation to zero. A protocol that only serves the wealthy is merely a digital version of the old “Walled Garden”. The culture mandate for the next generation of financial leaders is to view every ZK-Proof and every tokenized RWA as a brick in the “Invisible Bridge” to global equality.

The Collective Impact

The architectural move from shared ledgers to intelligent agents is more than a technical upgrade; it is a power shift. It represents the dismantling of the “Gilded Cage” of traditional banking, a system that has long prioritized extraction over universal access. By moving to open, active networks, we ensure that the math of wealth creation is identical for every human being on the planet.

The “Poverty Tax” is not a law of nature; it is a design choice. And design choices can be changed. When we replace bureaucratic discretion with smart contracts and natural language AI, we remove human bias from risk assessment and drastically lower the cost of financial participation. We are moving toward a 2030 where “financial freedom” is a technical guarantee, not a political promise.

In conclusion, the combination of blockchain’s immutable truth and AI’s agentic execution provides the terminal solution for financial inclusion. The walls of the old system are coming down. The bridge is being built. Ledger Impact will continue to analyze the architects of this future—those who understand that in the 21st century, the most powerful tool for social mobility is not a better bank, but a better architecture.

Citations and Sources

Federal Deposit Insurance Corporation (FDIC). (2023). National Survey of Unbanked and Underbanked Households. https://www.fdic.gov/analysis/household-survey/

Consumer Financial Protection Bureau (CFPB). Data Point: Credit Invisibles. https://www.consumerfinance.gov/data-research/research-reports/data-point-credit-invisibles/

European Parliament. (2023). Regulation (EU) 2023/1114 on Markets in Crypto-assets (MiCA). https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32023R1114

World Bank Group. (2022). The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19. https://globalfindex.worldbank.org/

Circle Official Reports. (2025). The State of the USDC Economy. https://www.circle.com/en/transparency

Decentralized Identity Foundation (DIF). Core Specifications and Architecture. https://identity.foundation/

International Monetary Fund (IMF). Financial Development and Inclusion. https://www.imf.org/en/Publications/fandd/issues/2016/june/caruana

Pew Charitable Trusts. Payday Loan Facts and the CFPB’s Authority. https://www.pewtrusts.org/en/research-and-analysis/reports/2016/05/payday-loan-facts-and-the-cfpbs-authority

Finovate News. (2026). 5 Things to Know about the CLARITY Act. https://finovate.com/5-things-to-know-about-the-clarity-act/

McKinsey & Company. (2023). Tokenization: A digital-asset déjà vu. https://www.mckinsey.com/industries/financial-services/our-insights/tokenization-a-digital-asset-deja-vu

The Brookings Institution. Economic Policy Research on the Poverty Tax. https://www.brookings.edu/topic/economic-policy/

Nakamoto, S. (2008). Bitcoin: A Peer-to-Peer Electronic Cash System. https://bitcoin.org/bitcoin.pdf

World Bank Group. (Ongoing). Remittance Prices Worldwide (RPW) Database.

https://remittanceprices.worldbank.org/