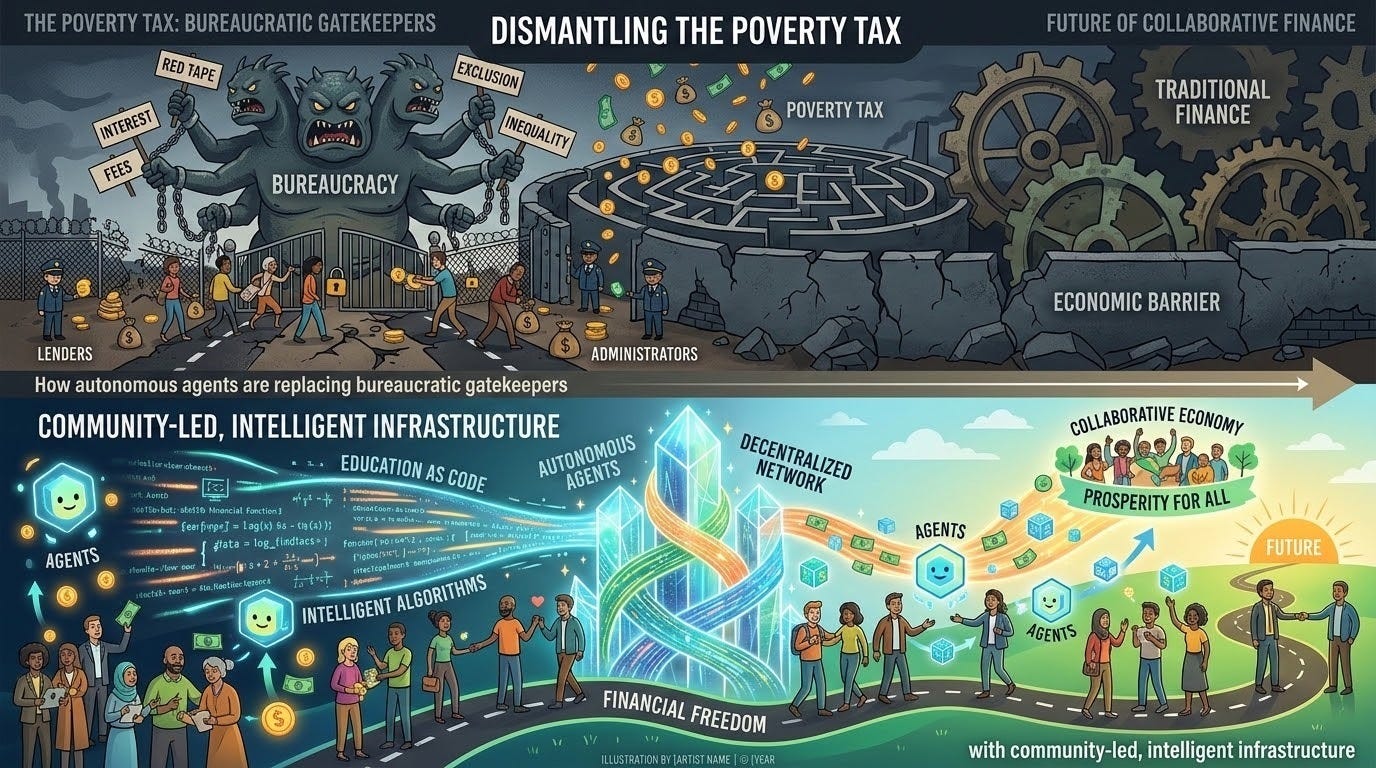

Dismantling the Poverty Tax: Education through Code and the Future of Collaborative Finance

Autonomous agents are replacing bureaucratic gatekeepers with community led and intelligent infrastructure.

The transition from passive and exclusionary banking systems toward an active agentic framework is rapidly accelerating. True financial inclusion is not merely about access to capital; it is about the synthesis of three critical pillars: affordable service, personalized education, and collaborative decision making.

We have reached a decisive tipping point. As of early 2026, research from Finastra indicates that 98% of financial institutions globally report utilizing artificial intelligence. This is no longer a fringe experiment but the fundamental infrastructure of the next century. We are witnessing the birth of a system where financial agency, long a privilege of the wealthy, is becoming a technical guarantee for everyone.

Macro Framework & The Education Gap

The “Poverty Tax” is not just a function of high fees; it is a function of information asymmetry. When financial systems are designed to be complex, those with the least resources are the most penalized by that complexity. The unbanked and underbanked have been trapped in a system that assumes high levels of financial literacy while simultaneously denying the tools to acquire it.

Even as digital finance becomes ubiquitous, the chasm remains profound. The World Bank’s Global Findex database reveals that 1.4 billion adults remain unbanked, locked out of the formal economy and vulnerable to economic shocks. For billions more—including gig economy workers, rural residents, and the “credit invisible”—a single unexpected expense can trigger a crisis.

Analysis indicates that the persistent failure of current digital banking is its reliance on static models. Consumers are often expected to navigate fluctuating interest rates and complex products with little context. To break this cycle, we must move beyond the basic digitization of Fintech 1.0 and adopt a more advanced model centered on personalized financial education through code.

Structural Deep Dive: The New Frontiers of Inclusion

Education as Code: From Passive Advice to Active Coaching

Financial literacy has historically been a static and top down curriculum. AI agents provide a revolutionary alternative through contextual financial coaching. By leveraging real time data from the blockchain, such as transaction history and savings behavior, an AI agent can deliver personalized financial education exactly when it is most effective.

New research from The Conference Board suggests that AI can provide up to 90% of day to day coaching functions, with 96% of workers reporting that AI provides customized and relevant guidance. This is transformative for financial inclusion. Instead of generic advice, an agent acts as a dedicated financial tutor:

Decision-Support: When a user considers a high-interest payday loan, the agent provides a side-by-side analysis of the “true cost” of that loan compared to alternative, lower-cost DeFi credit lines.

Behavioral Nudging: The agent identifies patterns where manageable adjustments in spending can lead to increased savings, guiding the user toward micro investments in tokenized Real World Assets. This transforms the user experience from reactive struggle to proactive planning.

Voice-First Inclusion: For populations with limited literacy, AI-powered voice interfaces in local dialects allow users to make payments and manage accounts without needing to navigate complex, text-heavy menus.

The Agentic Shift: Beyond Transactions to Agency

We are moving toward the AI powered financial copilot, an entity that does not just transact but also coaches, mediates, and governs on behalf of the user. Unlike standard models that wait for a prompt, agentic AI independently perceives, reasons, and acts without constant human guidance.

The market response is explosive. The global AI agents in the financial services market was estimated at USD 691.3 million in 2025 and is projected to reach USD 6,708.0 million by 2033, growing at a CAGR of 31.5%. Financial services executives are not waiting; 53% report they are actively using AI agents in production, with many deploying them for critical tasks like finance, accounting, and fraud detection.

This transition is fundamentally changing how we define “financial inclusion.” Inclusion is no longer just about assigning someone a bank account number; it is about enabling them to seamlessly interact with the full spectrum of financial services—transactional, savings, lending, and investment—all within a single, integrated experience.

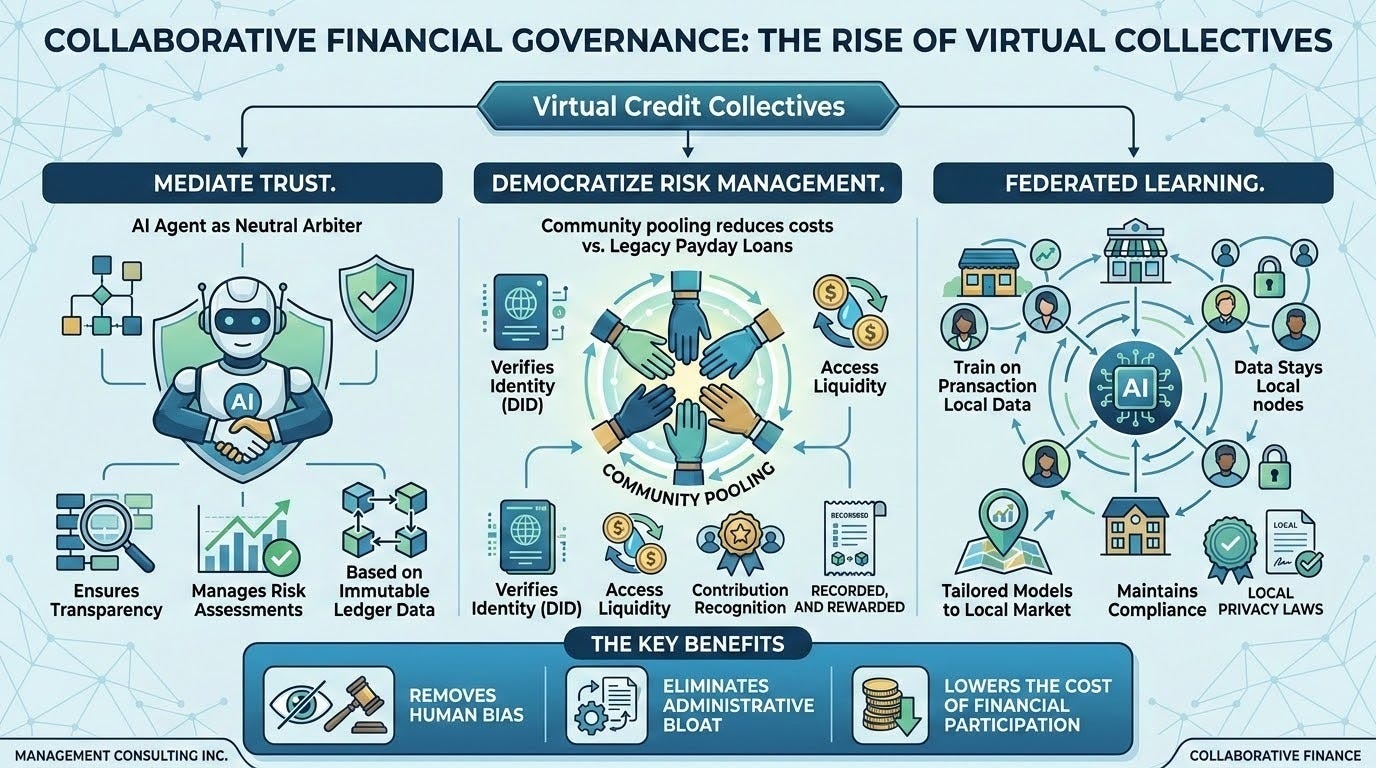

Collaborative Financial Governance: The Rise of Virtual Collectives

The most profound impact of agentic finance lies in collaborative decision making. We are entering an era of virtual credit collectives, which are community based financial governance models that function much like traditional lending circles but at a global and automated scale.

These collectives utilize autonomous agents to:

Mediate Trust: In a community-based lending circle, the AI agent acts as a neutral arbiter, ensuring transparency and managing risk assessments based on immutable ledger data.

Democratize Risk Management: By pooling resources, community members can access liquidity without the exorbitant costs of legacy payday loans. The agent facilitates the formation of these groups, verifies identity through Decentralized Identity (DID), and ensures that every member’s contribution is recognized, recorded, and rewarded.

Federated Learning: Innovations like federated learning allow AI models to be trained on local, private data (such as regional transaction habits) without moving sensitive data across borders, ensuring that models are tailored to local market realities while maintaining compliance.

This model removes human bias and the institutional gatekeeping that has long hindered community economic initiatives. By replacing bureaucratic discretion with smart contracts and natural language AI, we ensure fair risk assessment and drastically lower the cost of financial participation.

The Leadership and Culture Mandate

For founders and leaders, this shift requires a radical management pivot. We are no longer in the business of building “features”; we are in the business of training “agents.” This requires a shift from a product-centric culture to a system-centric culture.

Founders must prioritize the “credit invisible”—those ignored by centralized bureaus. This is not a charity play; it is a high-growth frontier. By using Decentralized Identity (DID) to verify transaction histories, founders can build a fairer credit scoring system where none existed before.

However, success requires a foundation of trust. Leaders must prioritize:

Explainable AI: Ensuring that both internal auditors and external customers can understand the logic behind an AI-driven decision is non-negotiable.

Bias Mitigation: Institutions must implement rigorous frameworks to detect and mitigate bias, ensuring algorithms provide fair and equitable outcomes across all demographics.

Data Stewardship: Consent-driven data usage is a prerequisite for customer trust. Customers must have clear control over their data and understand how it is being used.

The Collective Impact: Toward a 2030 Guarantee

The architectural move from shared ledgers to intelligent agents is more than a technical upgrade; it is a fundamental power shift. By moving to open and active networks, we ensure that the math of wealth creation is identical for every person on the planet.

The “Poverty Tax” is not a law of nature; it is a design choice. The IMF notes that AI is a “macro-critical transition” that calls for treating AI as a structural shift rather than a standard technology shock. We are moving toward a 2030 where “financial freedom” is a technical guarantee, not a political promise.

In conclusion, the combination of blockchain immutable truth, AI’s agentic execution, and the power of collaborative governance provides the terminal solution for financial inclusion. The walls of the old system are coming down. The bridge is being built. Ledger Impact will continue to analyze the architects of this future—those who understand that in the 21st century, the most powerful tool for social mobility is not a better bank, but a better architecture.

Citations and Sources

Federal Deposit Insurance Corporation (FDIC). (2023). National Survey of Unbanked and Underbanked Households. https://www.fdic.gov/analysis/household-survey/

Finastra. (2026). AI tipping point reached as just 2% of financial institutions report no AI use. https://www.finastra.com/press-media/ai-tipping-point-reached-just-2-financial-institutions-report-no-ai-use-finds-finastra

World Bank Group. (2025). The Global Findex Database 2025. https://www.worldbank.org/en/publication/globalfindex

The Conference Board. (2026). Research: AI Can Provide 90% of Career Coaching...But Humans Still Matter. https://www.conference-board.org/press/ai-can-provide-career-coaching-but-humans-still-matter

Grand View Research. (2026). AI Agents In Financial Services Market Report. https://www.grandviewresearch.com/industry-analysis/ai-agents-financial-services-market-report

International Monetary Fund (IMF). (2026). Global Economic and Financial Implications of Artificial Intelligence. https://www.imf.org/-/media/files/publications/imf-notes/2026/english/insea2026002.pdf

NVIDIA. (2026). State of AI in Financial Services Survey Report. https://www.nvidia.com/en-us/industries/finance/ai-financial-services-report/

Cambridge Centre for Alternative Finance. (2026). 2026 Global AI in Financial Services Report. https://www.jbs.cam.ac.uk/faculty-research/centres/alternative-finance/publications/2026-global-ai-in-financial-services-report/

OECD. (2025). Africa Capital Markets Report 2025. https://www.oecd.org/en/publications/africa-capital-markets-report-2025_7d26e1d3-en/full-report/harnessing-ai-in-finance-for-financial-inclusion-in-africa_a048b4fb.html