Breaking the Gilded Cage

Bringing High-Yield Assets to Every Household

Welcome back to the third installment of our series on the financial revolution. In our previous chapters, we dismantled the myths of legacy banking and explored the plumbing of the new digital economy. Today, we stand at the most exciting threshold of all: the democratization of yield.

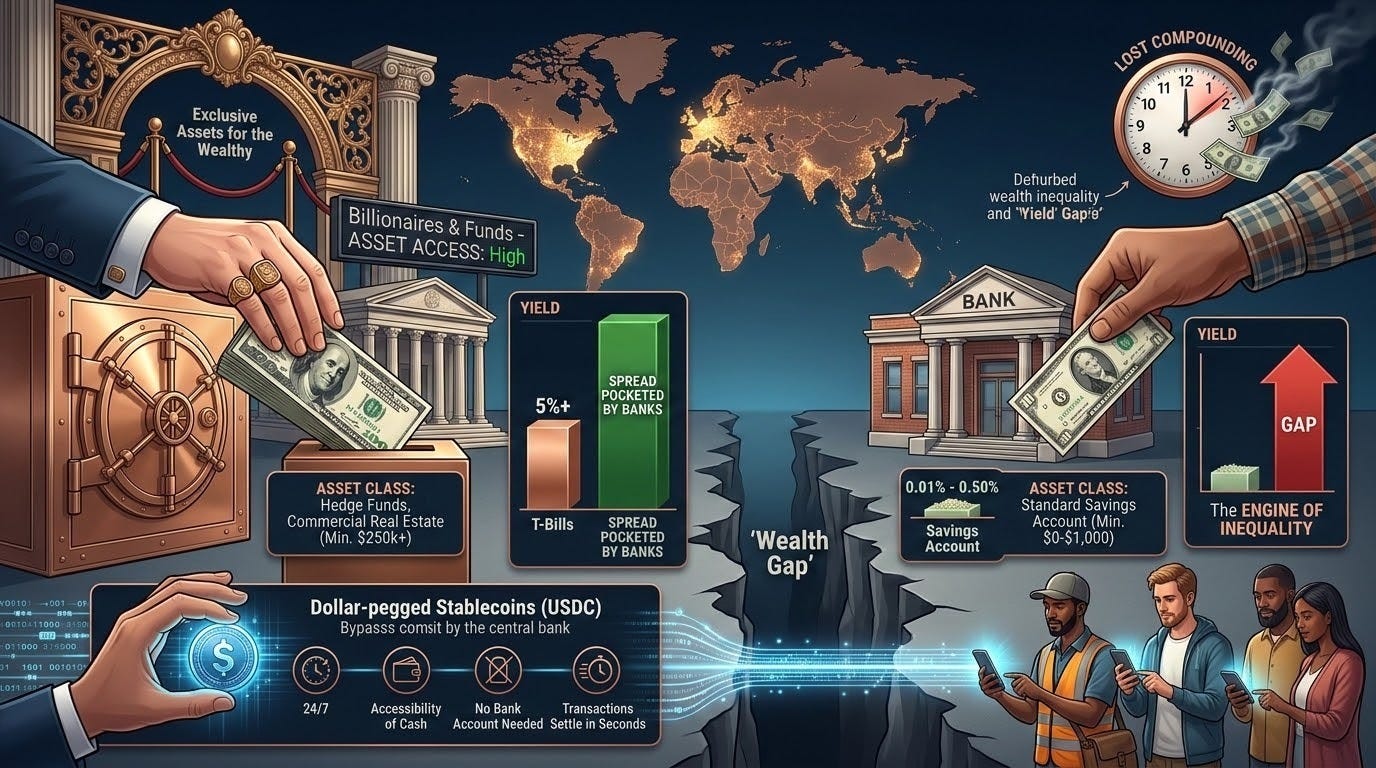

For decades, the global financial system has operated like a private club. If you had a million dollars, the doors swung wide, revealing a world of private equity, high-yield sovereign debt, and exclusive real estate trusts. If you had a hundred dollars, you were ushered into a waiting room where your savings languished in accounts yielding fractions of a percent, while inflation quietly eroded your purchasing power. This is the “Gilded Cage” , a system that keeps the majority of the world’s population locked in a cycle of stagnant growth while the elite compound their wealth at institutional rates.

But the bars are beginning to bend. We are witnessing the rise of Real World Assets (RWAs) on-chain, a movement that is effectively smashing the lock on high-yield opportunities and handing the keys to every household on the planet.

The Yield Gap Problem

To understand the solution, we must first confront the sheer magnitude of the disparity. The “Wealth Gap” isn’t just a catchy political slogan; it is a mathematical reality driven by asymmetric access to investment vehicles. According to the World Inequality Report 2022, the richest 10% of the global population currently owns 76% of all wealth, while the bottom 50% owns a mere 2%.

This is where dollar-pegged stablecoins like Circle’s USDC offer an immediate and powerful alternative. For gig workers, freelancers, or unbanked families globally, these assets function with the accessibility of cash but with the stability of a U.S. dollar deposit. They settle transactions in seconds, operate 24/7, and require no bank account to hold. This capability completely bypasses the traditional banking model that relies on charging fees and keeping the spread on low-yield savings accounts.

This gap is widened by what we call the “Yield Gap.” When the Federal Reserve raises interest rates, billionaires and institutional funds can instantly pivot into U.S. Treasury bills, often cited as the “risk-free rate”, earning 5% or more on their capital. Meanwhile, the average family, keeping their emergency fund in a standard savings account at a major commercial bank, often sees rates closer to 0.01% or 0.50%. The bank takes the family’s deposits, buys those same T-bills, pockets the 4.5% spread, and leaves the family with the crumbs.

Traditional Finance (TradFi) justifies this through “minimum ticket sizes.” To buy into a top-tier hedge fund or a commercial real estate development, you often need a minimum of $250,000 or even $1,000,000. These arbitrary barriers act as a velvet rope, ensuring that the highest-performing assets remain the exclusive province of the already wealthy.

The Yield Gap is the engine of inequality. By the time a middle-class family saves enough to meet an “accredited investor” threshold, they have already lost decades of compounding returns that could have secured their children’s education or their own retirement.

Fractional Ownership: The Great Equalizer

Enter the era of tokenization. By representing a physical asset—be it a T-bill, a skyscraper, or a fleet of cargo ships—as a digital token on a blockchain, we can achieve something revolutionary: infinite divisibility.

Through Real World Assets (RWAs), a family with just $100 can now bypass the gatekeepers. They are no longer limited to the “retail” products the bank decides to offer them. They can move directly into institutional-grade assets.

The Power Players Changing the Game

Several pioneering projects are already making this a reality:

Ondo Finance: Ondo is bridging the gap by bringing institutional-grade financial products to everyone. Their USDY (Yieldcoin) and OUSG products allow users to gain exposure to U.S. Treasuries. This means a freelancer in a developing nation can hold a stablecoin that earns the same sovereign yield as a Manhattan hedge fund manager.

BlackRock’s BUIDL: When the world’s largest asset manager enters the space, the “Gilded Cage” officially starts to crack. BlackRock launched the USD Institutional Digital Liquidity Fund (BUIDL) on the Ethereum network. While currently targeted at institutional players, it signals a massive shift toward a future where all high-yield funds are tokenized and, eventually, accessible via liquidity pools to the broader public.

Centrifuge: Centrifuge allows businesses to tokenize real-world assets like invoices or real estate and use them as collateral for loans. This creates a marketplace where individual investors can provide liquidity to small and medium enterprises, earning yields that were previously only available to specialized credit funds.

How it Works for the Everyman

Imagine a family in a suburb of Paris or a town in Ohio. They have $500 saved for a rainy day. In the old system, that money sits under a mattress or in a low-interest account. In the new system, they can purchase fractional shares of a tokenized apartment complex in a high-growth city or a basket of tokenized Treasury bills. The smart contract handles the distribution of rent or interest payments automatically. Whether you own 0.0001% of the asset or 10%, the yield per dollar is identical. That is the definition of financial equity.

DeFi as a Safety Net

Beyond just “making money,” the move to on-chain assets is about “keeping money safe.” The traditional financial system is notoriously opaque. We only need to look back at the 2008 subprime mortgage crisis or the more recent banking ripples in Europe to see how “shadow banking” and hidden liabilities can wipe out household savings in an instant.

Transparency as a Shield

In the predatory subprime lending markets of the past, banks bundled “junk” loans into complex products (CDOs) that even the buyers didn’t fully understand. When the foundation crumbled, it was the families who lost their homes and savings.

On-chain assets change the narrative through radical transparency. When an asset is tokenized and managed via Decentralized Finance (DeFi), every transaction, collateral ratio, and yield distribution is visible on a public ledger. There are no “off-balance-sheet” tricks. If a protocol like Centrifuge manages a pool of loans, an investor can see exactly what assets are backing that pool in real-time. This prevents the “smoke and mirrors” approach that defined the predatory lending era.

Programmable Money: The Advances of Circle and USDC

Circle’s USDC is at the forefront of this shift, having seen its circulation double significantly and processing over $28 trillion in transactions last year, surpassing the volume of major card networks. This scale and utility are transforming stablecoins from a crypto-periphery product to mainstream financial infrastructure. Critically, this technology is being built with regulatory clarity. The passage of the GENIUS Act in July 2025 established a gold standard for dollar-denominated stablecoins, mandating full 1:1 asset backing, transparency, and regular attestations for compliant issuers. Furthermore, recent guidance from the SEC defined stablecoins as a distinct category from “digital securities,” providing necessary clarity. While the FDIC has confirmed stablecoins do not qualify for deposit insurance, the required 1:1 reserve standard under the GENIUS Act provides a strict safety protocol, offering a higher standard of backing than fractional reserve banking.

Using DeFi protocols, a family can set up a system where:

Micro-Savings: 5% of every incoming payment is automatically converted into a yield-bearing RWA like Ondo’s USDY.

Automated Reinvestment: The yields earned are instantly compounded back into the asset without a human needing to click a button or pay a brokerage fee.

Emergency Liquidity: Instead of waiting 3-5 business days for a bank transfer, they can use their tokenized assets as collateral to take out a near-instant stablecoin loan for an emergency car repair, all while keeping their underlying investment intact.

This isn’t just a new way to trade; it’s a new way to live. We are moving from a world where you “go to the bank” to a world where “the bank is code” that lives in your pocket, works for you 24/7, and doesn’t care how much you have in your account.

Conclusion: The Horizon is Open

The “Gilded Cage” was built on the premise that complex, high-yield finance was too dangerous or too difficult for the average person. We were told to stay in our lane, accept our 0.5% interest, and let the “experts” handle the rest.

But the data doesn’t lie. The wealth gap is a structural problem that requires a structural solution. By tokenizing the world’s most valuable assets and placing them on-chain, we are removing the velvet ropes. We are ensuring that the same math applies to the $100 saver as it does to the $100 million fund.

This is Part 3 of our journey, and the message is clear: The tools for financial liberation are here. The transparency of the blockchain is our shield against predatory practices, and programmable money is our engine for growth. The cage is open. It’s time for every household to step out and claim their share of the global economy.

Stay tuned for Part 4, where we will dive into the regulatory landscape and how we can protect these new freedoms for generations to come.

Citations and Sources

Global Wealth Inequality: World Inequality Report. (2022). Data on global wealth distribution showing the richest 10% own 76% of wealth. [Source: https://wid.world/document/world-inequality-report-2022/]

USDC Transaction and Circulation Scale: Circle Official Transparency and Reports. Cited for significant circulation growth and processing over $28 trillion in transactions. [Source: https://www.circle.com/en/transparency]

Remittance & Yield Gap Data: World Bank Group. (Ongoing). Remittance Prices Worldwide (RPW) Database. Cited for the historical cost (5-10%) of cross-border transfers and the operational yield gap between institutional and retail savings. [Source: https://remittanceprices.worldbank.org/]

Real World Asset (RWA) Market Analysis: McKinsey & Company. (2023). Tokenization: A digital-asset déjà vu. Analysis on the market size, structure, and adoption of asset tokenization. [Source: https://www.mckinsey.com/industries/financial-services/our-insights/tokenization-a-digital-asset-deja-vu]

Institutional RWA Adoption (BlackRock BUIDL): BlackRock Official Statement/Filing. Announcement and structure of the USD Institutional Digital Liquidity Fund (BUIDL). [Source: https://www.blackrock.com/us/individual/products/333068/usd-institutional-digital-liquidity-fund]

Tokenized Treasury Fund (Ondo Finance): Ondo Finance. Product documentation for USDY (Yieldcoin). Cited as an example of retail-accessible RWA yield. [Source: https://ondo.finance/usdy]

Decentralized Asset Tokenization (Centrifuge): Centrifuge Documentation. Overview of tokenizing real-world assets (e.g., invoices, real estate) for collateral and lending. [Source: https://centrifuge.io/about]

SEC Regulatory Stance (Howey Test): United States Supreme Court. SEC v. W.J. Howey Co., 328 U.S. 293 (1946). Cited for the legal framework used to define digital asset securities. [Source: https://supreme.justia.com/cases/federal/us/328/293/]

US Regulator Clarity (Stablecoins): Office of the Comptroller of the Currency (OCC). Interpretive Letter 1174 (2021). Cited for guidance allowing national banks to use public blockchains and stablecoins for payment activities. [Source: https://www.occ.gov/topics/charters-and-licensing/interpretations-and-actions/2021/int1174.pdf]